A “new wave” of digital credit products has entered the digital financial services (DFS) market in recent years. These products differ from traditional credit by offering loans to borrowers that can be applied for, approved, and disbursed remotely (often without any brick-and-mortar infrastructure), automatically (generally minimizing or eliminating person-to-person interaction), and instantly (often in less than 72 hours). Digital credit also increasingly considers creditworthiness by using nontraditional data—ranging from mobile phone activity to utility payments and social media data—potentially allowing for loans to populations previously unable to access bank credit.

In EPAR Technical Report #351a: Review of Digital Credit Products in India, Kenya, Nigeria, Tanzania, and Uganda, we review the characteristics of 68 digital credit products identified in these five countries. The following dashboards present an interactive data visualization for our findings. See the table at the bottom of this page for definitions of concepts presented in the visualizations.

Digital Credit Products by Model, Country, and Year Established:

To view this visualization in full-screen, visit the Tableau page here.

Hover over specific data points on the figures to discover more information about what data and characteristics they represent. In order to focus the information presented in the charts on a particular variable, either: 1) select a category or a particular data point by clicking on the desired selection in the figure or legend (you can use CTRL to select multiple categories); or 2) select options from the right-hand filter menus. To revert back to a prior selection or reverse your last action, use the undo and redo buttons in the bottom left of the visualization. Clicking the reset button or a blank space in the selected chart will return the visualization to the standard view.

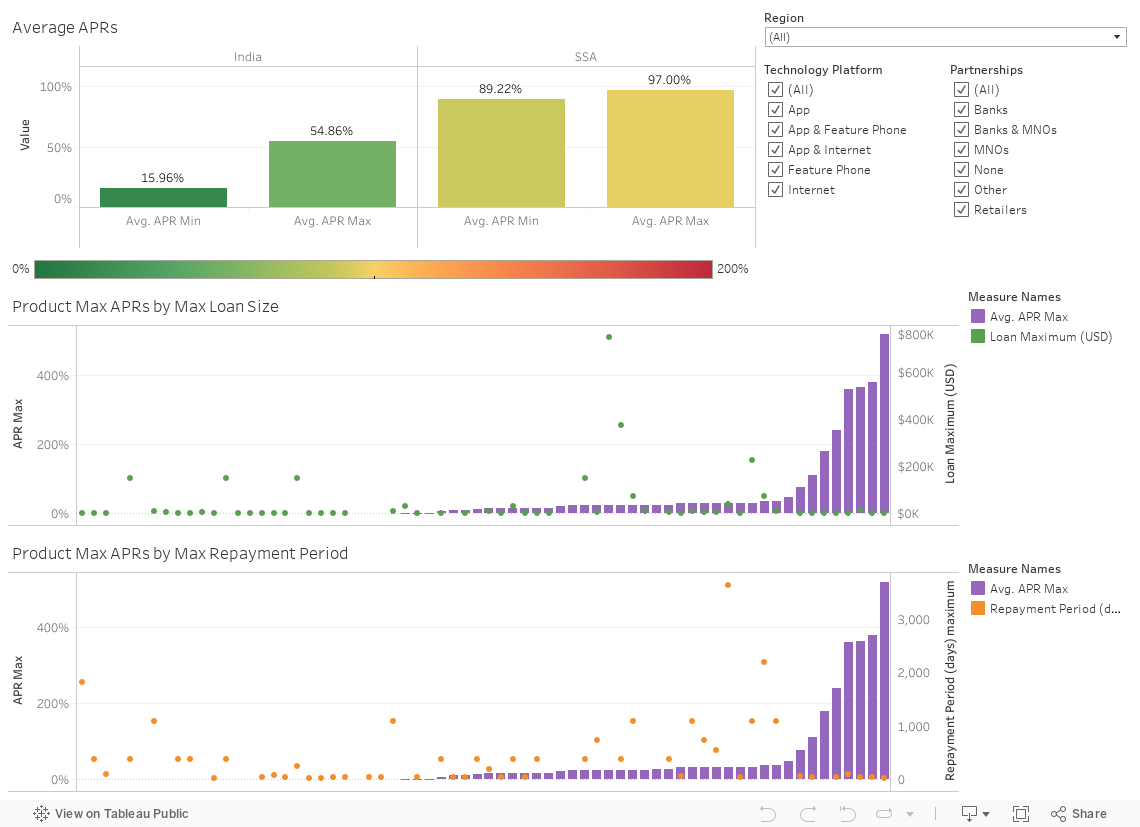

The Visualizations

These data visualizations, produced using Tableau, presents data on currently active digital credit products in India, Kenya, Nigeria, Tanzania, and Uganda identified through a series of web searches. The interactive figures allow for the exploration of relationships between various characteristics of these products.

The data used to produce these visualization are drawn from the websites of the individual digital credit products, supplement by information from grey literature searches. The dataset compiling all of the information retrieved for each product and our report presenting our analysis of the data are available for download here.

Definitions

| Standard Model | Products disburse loans as electronic value to customer’s mobile money wallet or bank account; loans are unsecured and are provided by banks, MNOs, or big lenders, not individuals |

| P2P Lending Model | Products connect borrowers with individual private lenders, where lenders provide the funds and the P2P products provide the platform for borrowers and lenders to meet and exchange funds. |

| Retail Model | Products allow consumers to apply for a loan in order to purchase products such as cell phones, computers, and other high-cost personal items. |

| Other | Products do not fit clearly into standard, P2P, or retail categories. |

| Technology Platform | The channels through which customers access and use a digital credit product. These include internet websites, feature phones (non-internet enabled phones), and smart phone apps. Most products use a single technology platform, but some offer products on two platforms. |

| Partnerships | Digital credit providers that have partnered with other organizations, including banks, mobile network operators (MNOs), retailers, and other partners, such as non-bank financial institutions or investment firms. |

| Alternative Data Types | The majority of the digital credit products we reviewed (52 out of 68) used their own scoring algorithm to determine creditworthiness, and the rest mentioned partnerships with third-party credit score start-ups. Most products’ websites described the types of consumer data used in their algorithms. We sorted the types of data used for alternative data scoring into six categories: mobile money data, mobile phone data, online activity and social media, other personal information, previous digital credit loans, and traditional financial history. |

| Customer Targeting | Many of the products in our review state that they target one or more particular customer segments. The most commonly mentioned target populations are small business owners, urban borrowers, and low-income borrowers. None of the products we reviewed states that they target rural borrowers or farmers, and only one product states that it targets female borrowers (though that product did not use alternative data to generate credit scores). |

| Loan Terms | Almost two thirds of the digital credit products we reviewed (44 out of 68) report the annual percentage rates (APR) of interest they charge on loans, often specifying minimum and maximum APRs charged to customers with different credit ratings. The digital credit products also vary in terms of the maximum loan amount they are willing to offer, and the maximum length of the loan repayment period. |

By Daniel Lunchick-Seymour

Summarizing research by Pierre Biscaye, Kirby Callaway, Melissa Greenaway, Daniel Lunchick-Seymour, Max McDonald, and Professors C. Leigh Anderson, Marieka Klawitter, and Travis Reynolds